4.1 Relevance of intergovernmental fiscal transfers

Intergovernmental fiscal transfers are the primary source of revenue in a majority of countries around the world, on average accounting for over slightly over half (51 percent) of total subnational government revenues, or 4.2 percent of GDP (OECD/UCLG 2019: 70). However, there are considerable variations in the magnitude of intergovernmental fiscal transfers across countries, both in terms of absolute size as well as in terms of their share in total subnational revenues. While intergovernmental fiscal transfers play an important role in both urban and rural local governments, the role of transfers is often more dominant in rural local governments that may have a limited taxable economic base of their own.

It is important to acknowledge that the importance of intergovernmental fiscal transfers is not a coincidence or a temporary situation. Instead, in almost all countries, we should expect a permanent “primary” vertical fiscal imbalance, a situation where subnational expenditure needs exceeding subnational own source revenues, before intergovernmental fiscal transfers are taken into account (Hunter 1977). This structural imbalance is due to the fact that the extent of optimal expenditure decentralization is consistently greater than the optimal level of revenue decentralization, when the subsidiarity principle is applied to both. As such, an important raison d’etre for intergovernmental fiscal transfers is to help to reduce this vertical fiscal imbalance or gap. Another reason for intergovernmental fiscal transfers is to ensure an equitable horizontal distribution of resources, typically by making sure that localities with greater expenditure needs or lower own revenue potential receive greater transfer allocations.

4.2 An overview of intergovernmental fiscal transfers

What are intergovernmental fiscal transfers? Intergovernmental fiscal transfers (IGFT) include a wide range of fiscal instruments by which funds are transferred from one government unit – often at a higher government level – to another government unit often at a lower government level. Sometimes IGFT are referred to as grants or intergovernmental expenditures by the “giving” government, and as intergovernmental revenues by the recipient government. Many other (often country-specific) terms are used to describe different types of intergovernmental fiscal transfers, including general allocations, equitable shares, subventions, and subsidies.

Intergovernmental fiscal transfers or intergovernmental expenditures are different from other “direct” government expenditures or outlays based on the fact that there is no immediate quid pro quo. While the recipient government may (or may not) have to fulfill certain conditions to receive fiscal transfers, the provision of transfers is generally not a final payment for specific goods or services rendered—as is the case, for example, with wage expenditures or the purchase of goods and services or capital infrastructure.[22] On the revenue side, intergovernmental fiscal transfers differ from other own revenue sources in that the recipient government does not have any control over the rate, base or collection of intergovernmental fiscal transfers.

Types of transfer schemes. The actual nature of IGFT schemes varies greatly, both across and within countries. Some, such as revenue sharing schemes are accounted for on the revenue side of the budget. But most transfer schemes are recorded on the expenditure side of the central government budget, which may include general-purpose (unearmarked or unconditional) transfers or grants, as well as categorically earmarked transfers or “block grants” and specific/earmarked grants (Figure 4.1).[23][24]

In addition to the variations in transfer-related terminology, which often differs from country to country, there is no single consistent approach or typology to classify IGFT schemes (Hunter 1977; Bahl and Linn 1992; OECD 2013; Boadway and Eyraud 2018). Most of the typologies used to classify different types of transfer schemes consider some combination of five elements of transfer design. These are:

- The nature and manner of determining the size of the transfer pool or vertical allocation—for example, rule-based vertical allocation versus discretionary vertical allocations, on-budget or off-budget, and revenue-sharing versus budgetary transfers.

- The manner or nature of determining the horizontal allocation of the transfer resources—for example, formula-based horizontal allocations versus discretionary horizontal allocations; equalizing versus non-equalizing.

- The extent and nature of or earmarking imposed on the transfer—for example, unconditional or general-purpose grants versus more conditional or earmarked grants such as categorical grants or specific grants.

- The economic (incentive) nature of the transfer—for example, matching grant or partial reimbursement versus non-matching grant/full reimbursement.

- The existence of “performance-based” access conditions (or incentives) and other conditions relating to the management of grants—for example, requirements related to the planning, budgeting, and use—as well as the reporting on the use—of transfers).

While elements the last three listed types define the level of conditionality associated with transfer schemes, all categorical and specific grants impose some degree of conditionality and are generally referred to as conditional grants.

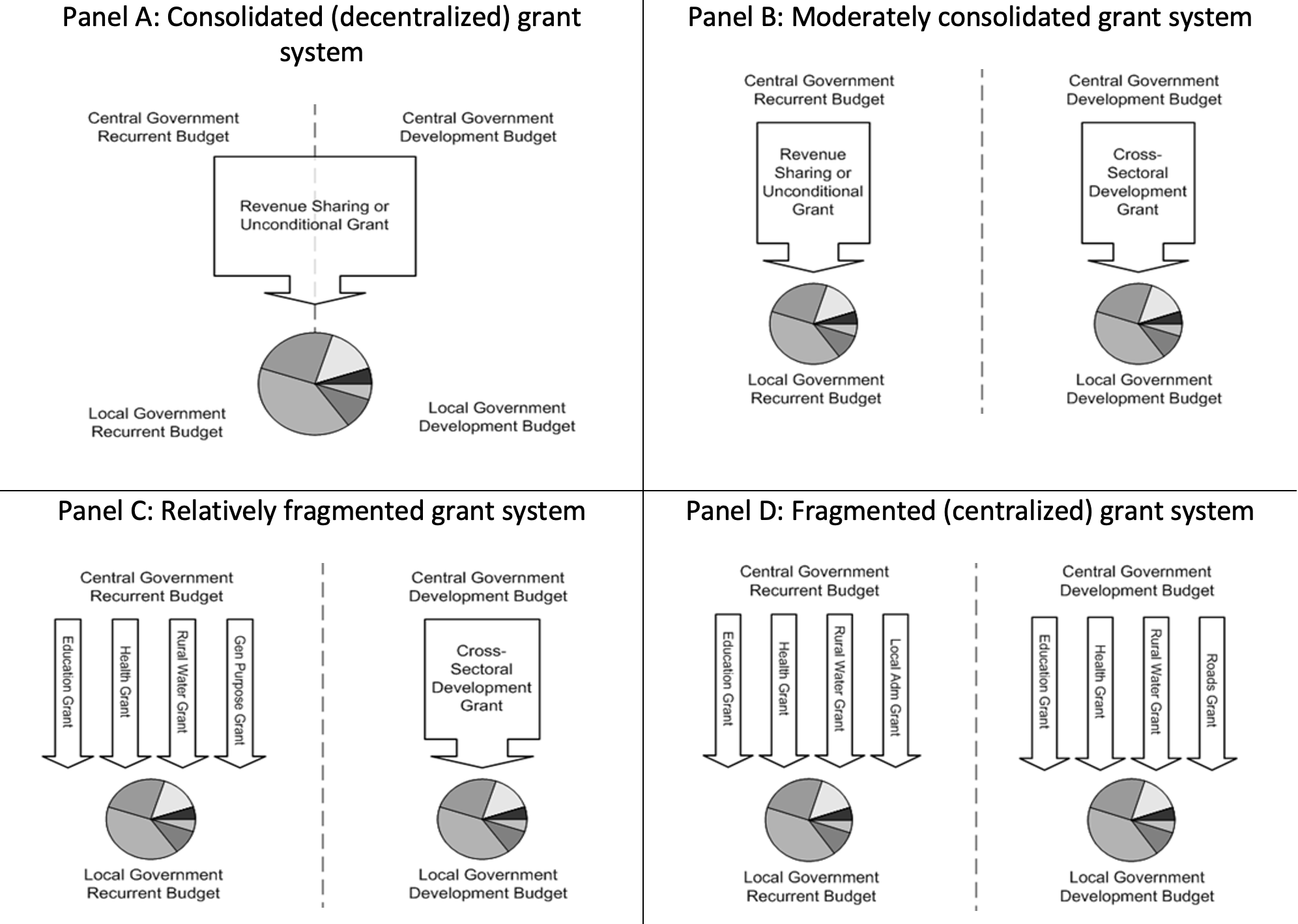

Types of transfer systems. In addition to acknowledging the wide range of IGFT schemes that can be designed and implemented, it is useful to recognize that the composition of IGFT systems ranges widely around the globe. As shown in Figure 4.2 (next page), these systems can be modulated by policy makers from a highly consolidated transfer system –comprising one large unconditional funding flow with extensive subnational or decentralized decision-making power and control – to a highly fragmented transfer system, with a large number of often highly conditional intergovernmental funding flows allowing for extensive centralized control.

There is no single, universal “better” international practice when it comes to IGFT systems. In some cases, especially to the extent that subnational governments perform effectively as inclusive, responsive, and accountable mechanisms for subnational decision making and services delivery, a highly unconditional grant system might result in effective public sector performance, as in Germany. The same transfer system under greater institutional constraints with respect to political and administrative systems is likely to perform more poorly as experienced in Nigeria. Many countries, such as Indonesia, Kenya, and South Africa try to avoid an excessive conditional grant system and opt for a mix of general-purpose and conditional grants. At the same time, some federal countries like the United States that are generally considered highly devolved rely on highly fragmented and earmarked transfer systems.

Fragmentation of the transfer system often results in a multiplicity of schemes—each often with their own minimum access conditions, spending requirements, disbursement triggers, and reporting requirements. This often strains the ability of local government officials and local financial management systems to manage different funding flows. More often than not, development partner projects contribute to this fragmentation and complexity rather than help resolve it. In addition, as further discussed below, formal IGFT schemes often operate alongside non-devolved vertical funding mechanisms, thus resulting in a reality far beyond the neat linear funding arrangements implied by the diagrams in Figure 4.2 above.

The key to unlocking the power of subnational governments. In public policy discussion of transfer schemes the horizontal allocation formula almost always gets most of the attention. But in reality, it is actually the increase in fiscal space associated with the vertical allocation (the size) of transfers that unlocks the power of local governments, simply by providing local governments with greater financial resources to do more things that they could not afford based on their own revenue sources alone. By providing a binding (“hard”) budget constraint, a well-designed transfer system has the potential to greatly improve the allocative efficiency of the public sector. This is effected by strengthening public sector planning and transforming the planning process from the preparation of unaffordable or poorly prioritized wish lists, to a system within which local officials are required to meaningfully prioritize and plan their expenditures in a results-based manner.

In addition, transfers can further be used in more strategic ways. For instance, different types of conditional grants – categorical or specific grants and matching grants – can be used to encourage local governments to increase their spending on specific functions, such as concurrent functions, or tasks that might otherwise be underfunded. Also, well-designed transfer schemes—in particular, performance-based grants—can be used to provide specific carrots and sticks for local governments, for instance, to improve local governance arrangements, or to improve local service delivery outcomes.

Universal principles. Over the years, experienced policy practitioners and analysts of fiscal decentralization have arrived at a list of a dozen or so universally accepted principles of sound transfer design (Bahl and Linn, 1992; Shah, 1995; Martinez-Vazquez and Boex, 2001). Although the exact number of points and the phrasing of the individual points vary slightly among different sources, these universal principles are commonly accepted as important guidance in designing an effective grant system (Table 4.1).[25]

| Principle | Clarification |

|---|---|

| 1. Clear objective | The allocation should be guided by a clearly stated policy objective. |

| 2. Revenue adequacy | Transfers should provide adequate resources for purpose at hand (and avoid unfunded mandates). |

| 3. Preserving budget autonomy | Conditions placed on transfers should balance national priorities and local autonomy. |

| 4. Enhancing equity and fairness | The transfer mechanism should support a fair allocation of resources. |

| 5. Stability | The allocation should be stable and predictable over time. |

| 6. Simplicity and transparency | The transfer mechanism should be simple and transparent. |

| 7. Incentive compatibility | The allocation approach should not provide negative incentives. |

| 8. Focus on service delivery | Transfer formulas should focus on the demand (clients or outputs) rather than the supply (inputs and infrastructure) of local government services. |

| 9. Avoid excessive equal shares | Excessive reliance on the “equal shares” principle as a major allocation factor should be avoided. |

| 10. Avoid sudden large changes | Avoid sudden large changes in funding for local governments during the introduction of the new transfer mechanism. |

4.3 An overview of non-devolved subnational funding flows

By definition, IGFTs include only the funding flows such as general revenue sharing or grants-in-aid between two government units which, in many cases, means the central government as the funder and a local government as the recipient. Indeed, virtually all discussions and analyses of IGFTs limit themselves to these transfers. In reality, however, as illustrated earlier in Figure 2.3, numerous different types of non-devolved vertical or intergovernmental funding flows operate alongside IGFTs.

Although there is little available on systematic quantitative analysis of non-devolved funding flows, the most common non-devolved subnational funding flows (or quasi-transfers) are likely to include:

- Centralized spending on local public services. In some countries, different aspects of local frontline services are provided and/or funded directly by central government ministries, often through national vertical or sectoral programs. For instance, in Bangladesh, the majority of frontline health services—including the salaries of health workers—are managed and funded under the central government’s budget vote by the Directorate General of Health Services, Health Services Division. Even in countries such as Sierra Leone, where local health services are de jure a local government function, it is not unusual for frontline health workers to be employed by the central government. In other countries like Tanzania, where recurrent health services are provided in a devolved manner, the construction of new health facilities may be funded from the central ministry budget, alongside the provision of sectoral block grants and other sectoral transfers to the local level.[26] This category of fund-flows also includes grants to service providers that are not formally part of the public sector, such as grants from the Ministry of Forestry to Forest User Groups in Nepal, or funding support by the central Ministry of Water to local water user associations or committees. It is often difficult to disentangle how much national program spending actually reaches the front line.

- Deconcentrated spending on local public services. A second non-devolved funding flow includes deconcentrated spending on local services. As opposed to the previous example, under budgetary deconcentration, the subnational departments or offices are separate budget organizations, units or cost centers in the budget, and are therefore easier to identify. For example, in Egypt’s national deconcentrated budget structure, the funding provided for the basic services delivered by governorate-level sectoral directorates are not contained in the central ministry budget, but rather, in separate, dedicated budget votes for these directorates.[27] In other countries, deconcentrated funding streams operate alongside centralized and/or devolved funding flows. For example, in Bangladesh where, as noted, health programs are largely delivered in a centralized manner, Upazila subdistrict Health Offices and Upazila Health Complexes are operated and funded by the Health Services Division in a deconcentrated manner, rather than as part of the Directorate General of Health Services.

- Funding support from national parastatal entities, funds, and authorities. Sometimes, local governments, or alternatively local-level facilities or service delivery providers receive funding support from national parastatal entities, funds and authorities. This may include resource allocations to local governments for road maintenance from the Roads Funds, as in Tanzania; payments to local health facilities for maternal health services from the National Health Insurance Fund (“Linda Mama”) in Kenya; or allocations from sectoral trust funds or investment authorities, as with grants from the Water Sector Trust Fund to county governments in Kenya. In these cases, the funding entity is typically an extrabudgetary entity at the central government level, while the receiving entity may be either be a local government or a non-devolved local entity. Due to the partial or full off-budget nature of these transactions, depending on which data sources are being used (central or local), it may be easy to overlook these transfers or grants.

- Provision of frontline services by national parastatals, funds, and authorities. In other cases, national parastatals, funds, and authorities or even donor partners may provide in-kind inputs in support of local public services, rather than a flow of funds. For example, rather than receiving funding from the Medical Stores Department (MSD), local governments may receive a notional budget or account from MSD against which they can “purchase” medicines, which are then delivered in-kind. Similarly, local agriculture departments may get seeds and fertilizer through in-kind distributions, rather than fiscal transfers.

| Box 4.1 Grants funded by international financial institutions and development partners Intergovernmental fiscal transfers can be a good entry-point for international financial institutions and development partners to support improved subnational governance or improved subnational service delivery. When they use this entry-point for policy reform, development partners should avoid standalone projects. Instead, they should design funding modalities to align with the country’s transfer system whenever possible and ensure that the funding mechanism being introduced is a sustainable part of the country’s long-term intergovernmental fiscal architecture. When possible, development partners should provide funding support in an on-budget manner as a top-up to existing grant schemes, rather than introducing parallel funding streams that contribute unnecessarily to the fragmentation of the grant system and increase the administrative burden on local officials. When this is not possible, the second-best option is to provide create a new on-budget grant modality—for example, a sector grant supported by a multi-donor trust fund under a sector-wide approach. Only as a last resort should development partner grants bypass the national government and be deposited straight from donor-controlled project accounts into local government accounts or, even worse, pay local contractors directly for services rendered to the local government, thus bypassing central and local public sector systems altogether. |

Because most “devolved” countries actually rely on a combination of devolved and non-devolved service delivery institutions and funding approaches, it is critical to consider and analyze the reliance on non-devolved grants and (quasi-)intergovernmental fiscal transfers in order to achieve a solid understanding of the intergovernmental fiscal context.

4.4 Common obstacles in intergovernmental fiscal transfers: technical challenges

Intergovernmental fiscal transfers are a relatively blunt instrument of intergovernmental finance. The importance of IGFT to intergovernmental finances notwithstanding, it should be recognized that, in practice, transfers are actually a relatively blunt policy tool, as local governments and local government officials—as rational economic agents—tend to respond to receiving different types of grants, sometimes in helpful ways, and sometimes in ways that undermine the performance and accountability of the public sector.

For example, when local governments are provided with additional unconditional grant resources to a local government, it is common for local leaders to react by reducing local tax collections in response to the increase in grant resources, doing so in response to the preferences of their local constituents.[28] This means that for every hundred dollars in unconditional grants provided, spending will increase by less than a hundred dollars. Furthermore, it is unlikely that the local government will direct these resources towards central government priorities. In fact, it should be expected that local officials will spend any additional general-purpose resources on local priorities. While such political responsiveness may not be appreciated by the national fiscus, this is simply a rational economic choice for elected local government officials in response to an expanding budget constraint.[29]

Similarly, whereas sectoral (block) grants or specific grants may be provided by the central government in order to achieve a specific national policy objective, it is important to be aware that local governments may decide to reduce their own spending from general-purpose funds in support of this function when a conditional grant is introduced—for example, in favor of spending programs deemed to be in higher need of the marginal dollar. Likewise, unless spending from conditional grants is carefully monitored, it would not be unusual for local governments to “accidentally” spend resources outside the menu of permitted expenditures. Again, given that the public sector is often underfunded, and given that performance metrics are often difficult to validate, which is true in every country, but especially in countries with weaker public administration, it should not be surprising if local public officials over-report certain data, such as enrollment, a number related to health attendance. if doing so would help them attract greater funding for the purpose of improving local service delivery. For performance-based grants: results results may be overstated for the same reason.[30]

Another concern in the design of IGFT is a misalignment of expectations associated with the grant system. Expectations can misalign in a number of different ways. A first common misalignment in expectations is known as the “tragedy of the commons,” which occurs when a local government is allocated an unconditional grant and, in response, every central sector ministry expects that the local government will allocate these resources to fund its (ministries’) sectoral services and programs. When this happens, a strain will be put on the intergovernmental (fiscal) system as a whole: sector ministries will under-provide conditional sector grants, local government services will be underfunded across the board, and local governments will systematically fail to achieve the results that are set by central government ministries.

A second misalignment in expectations takes place when the central government allocates unconditional grants in a pro-poor manner to local governments by using the number of poor residents in each locality as an allocation factor, and expects local governments to spend these resources on pro-poor programs. In reality, however, the inclusion of a poverty variable in the allocation formula has no bearing on whether local governments will spend these resources in a pro-poor manner.

A third misalignment in expectations takes place when central government designs a conditional grant scheme – for example, a performance-based grant program that requires the recipient to abide by numerous central government conditions – but then provides inadequate funding to give a meaningful fiscal incentive to local administrators and decision-makers to adequately implement the conditional grant program. The local government may accept the grant while resenting the conditions being imposed, and the central government will end up complaining that local governments are incompetent or dragging their feet.

Beyond the concerns noted above, there are a number of common challenges, including:

- The structure of the transfer system is unclear or is excessively fragmented and conditional. It is not unusual for the grant system to lack a clear link between the functional responsibilities to be funded and the composition and size of the various transfer mechanisms. A failure to achieve an appropriate balance between unconditional and conditional grant instruments places unnecessary restrictions on local budget autonomy, often resulting in reduced allocative efficiency.

- The process or timing of intergovernmental budget formulation process. One of the most important benefits of fiscal decentralization is that it requires local governments to plan and prioritize in the context of a hard budget constraint. But, if the central government fails to set grant ceilings in a timely manner as part of the central government’s budget formulation process – or if the central government changes grant ceiling after issuing the local budget circular – local governments are unable to prepare their plans and budgets in an in effective, inclusive, and accountable manner.

- Problems with vertical and horizontal allocation. The vertical allocation of resources may be inadequate to achieve the required service delivery objectives. The horizontal allocation of resources may also be fair or inefficient. For example, some local governments may receive relatively more resources than needed for their expenditure needs compared to other localities.

- Disbursement problems. Transfers should be disbursed in a complete, consistent and timely manner. It is not unusual, however, for central governments to fall short in this regard, due to poor planning or weak cash management. In other cases, the complexity of disbursement procedures causes delays. In fact, it is not unheard of for grant releases to be made on the last day of the financial year. The failure of the central government to disburse committed resources in a timely manner can cause considerable downstream problems such as low budget performance, unpaid local government staff, and delays in contracting.

4.5 Political economy considerations: common obstacles in intergovernmental fiscal transfers

Empowering intergovernmental (fiscal) systems: intergovernmental fiscal transfers. While the design of IGFT systems and schemes is a highly technical exercise, the issue is highly political at the same time. After all, there is nothing more political than the allocation of public resources to competing demands. In fact, political economy forces permeate not only specific decisions regarding the vertical and horizontal allocation of resources, but also the design of the grant system as a whole. This includes decisions regarding the mix of conditional versus unconditional grants and the choice of formula-based versus discretionary grant schemes).

While a neutral observer would balance the pros and cons of conditional versus unconditional grants or judge the technical merits of formula-based versus discretionary grant schemes, central government officials are likely to have an institutional or even personal stake in deciding on the nature of the grant system. While formula-based grants may be preferred on technical grounds – due to their objectivity, predictability, transparency – the choice of grant instruments itself may be determined by a contestation of power, both within and between political parties as well as within and between different ministries. Powerful members of parliament or powerful mayors may prefer that the bulk of resources is provided through more discretionary allocation mechanisms rather than rules-based and formula-based transfers, which would allow them greater control over the allocation of resources by lobbying the Minister of Finance or other relevant ministries, such as the ministries responsible for local government or urban development. Representatives of politically weaker jurisdictions may prefer a formula-based approach, which—while limiting their own discretionary power—could ensure a more favorable distribution of resources for their constituencies. The Minister of Finance may prefer to have discretionary control in setting the total pool of funds transferred to subnational governments from year to year, rather than using a predictable vertical sharing rule, which would provide more stability for local governments, but would give the Minister fewer tools to ensure macro-fiscal stability. Similarly, central sector ministries may prefer conditional sectoral grants over unconditional grant schemes, especially if the grant is located within the ministerial budget votes, and gives ministry officials the power to approve or decline disbursements based on whether conditions have been met. Therefore, as a result of the political economy forces, there is a tendency for transfer systems to become increasingly fragmented over time, as national actors and many development partners have a desire to exercise control and oversight over funding flows to the local level through conditional grants.

Once the structure and nature of the grant system has been decided, the actual vertical allocation of resources, typically determined as a part of the central government’s annual budget formulation process, is again subject to political economy forces. Determining the size of the various transfer pools should be informed by the desire to provide adequate funding based on the policy objectives of the grants in a way that balances the financial needs of local governments with those of central ministries. But, in most countries, the vertical allocation decision is ultimately a policy decision made by Cabinet—by political representatives leading central government ministries. In order to (partially) counteract potential bias in the vertical allocation of resources, some countries have constitutionally or legally put in place different intergovernmental institutions, such as India’s Finance Commission, Kenya’s Commission on Revenue Allocation (CRA), or Nepal’s National Natural Resource and Finance Commission (NNRFC), to be a more neutral arbiter of vertical fiscal balance.

Even when a formula-based approach is selected, rather than a more discretionary horizontal allocation approach, it is important to recognize that the presence of a formula-based allocation mechanism does not assure that the horizontal allocation of resources is necessarily objective or fair. After all, it is typically central government bureaucrats who prepare the proposals for grant allocation formulas, while central government politicians hold the power to enact or reject the formula-based allocations of transfer resources. For instance, if powerful politicians from wealthier jurisdictions have a stronger voice in parliament, equalizing grants may face a higher political hurdle, while matching grants, which may cause wealthier local jurisdictions to receive greater transfers. would be more favorably received.

A number of studies have been done on the political economy of transfer allocations over the years, looking specifically at the horizontal incidence of IGFT across different local governments. The collective findings of the literature suggest that while normative considerations and voter choice considerations are often significant forces in the distribution of transfers, political factors are consistently a major driving force in determining the horizontal incidence of IGFT in fiscally decentralized systems around the world (Boex and Martinez-Vazquez 2004). Recognizing the fact that the development of grant allocation formulas is not merely a technical exercise—but that politicians have to approve the resulting grant formulas, and that they will view the formula through a political economy lens—requires policy analysts and technical experts to “think political.” This means that though the mandate of policy analysts and development practitioners is purely technical, it would be counterproductive to ignore who the main “winners” and “losers” would be from the introduction of a new grant program or from the change in an existing allocation formula.

Efficient, inclusive and responsive local governance: intergovernmental fiscal transfers. In almost all cases, IGFT are provided to encourage changes in the choices made by local government officials. In some cases, transfers have the intended effect; for example, a sectoral block grant may result in improved service delivery outcomes. In other cases, grants may have unintended consequences; for example, an unconditional grant may lower own source revenue collections.

The exact impact of IGFT on the political and budgetary decisions at the local level is highly context-specific, and depends on the exact nature of the transfer or transfers provided to the local government level—unconditional, conditional, or performance-based. How local governments respond to fiscal incentives provided by higher-level governments depends on how elected local officials, local administrators, and frontline service providers balance the various demands placed on them from different directions, and in some cases, on the nature of the intergovernmental fiscal transfers. For instance, if wage grants are provided as part of a sector block grant, this may provide local governments an incentive to hire workers that provide high value-for-money, and to replace non-performing workers. The decision to terminate weak performing staff may be different if wage grants are explicitly tied to the salaries of workers being sent from the sector ministries. Thus, terminating an underperforming worker would result in a decrease in the wage resources made available.[31]

A final observation regarding the political economy of IGFT deals with an argument made by some observers that local governments are more likely to spend transfer resources in a more frivolous manner when compared to funding that was collected from local taxpayers. While this may be true in certain cases, local government leaders may also waste own source revenues unless political accountability mechanisms are strong and effective. In the end, the effective use or misuse of intergovernmental fiscal transfers will depend on the vertical as well as the horizontal context within which these resources are placed.

| Box 4.2. Further background and resources on intergovernmental fiscal transfers – Intergovernmental Fiscal Transfers: Principles and Practice. Robin Boadway and Anwar Shah: World Bank 2007. – Fiscal Equalization in OECD Countries. Hansjörg Blöchliger, Olaf Merk, Claire Charbit, and Lee Mizell: OECD Fiscal Federalism Studies 2007. – Fiscal Equalization: Challenges in the Design of Intergovernmental Transfers. Jorge Martinez-Vazquez and Bob Searle, eds.: Springer 2007. – Designing Sound Fiscal Relations Across Government Levels in Decentralized Countries. Robin Boadway and Luc Eyraud: IMF 2018. – Conditional Grants in Principle, in Practice and in Operations: A Toolkit. World Bank 2022. |

[22] In fact, in the case that one government unit directly purchases a good or service from another government unit, the nature of the transaction changes, so that such a transaction would no longer be classified as an intergovernmental fiscal transfer (U.S. Census Bureau 2006).

[23] Despite shared revenues sometime being classified as own revenue sources in the Chart of Accounts of different countries, as noted above, public finance economists tend to consider shared revenues as IGFT when the recipient government does not have any control over the rate, base, collection or sharing rate of the shared revenue source.

[24] Categorical or block grants are conditional grants that are required to be spent on a specific spending category, but otherwise allow the recipient a degree of discretion on how to spend the grant resources. For instance, a cross-sectoral capital development grant or a local education sector grant can be provided as a categorical grant, allowing the recipient government a degree of autonomy, as long as the resources are spent within the relevant sector or spending category. A specific or earmarked conditional grant allows the recipient government little or no spending discretion. For instance, specific earmarked grants may be used to pay for specific infrastructure projects approved by the central government, or pay for the wages of filled staff positions, as approved by the central government.

[25] Although subnational budget allocations in Egypt are technically not intergovernmental fiscal transfers, as governorates are deconcentrated entities rather than autonomous local governments, much of the literature on intergovernmental fiscal transfer design applies.

[26] In many countries, development partner-funded investments in sectoral infrastructure are made through centrally managed programs, even when the provision of sectoral services is legally devolved to the local government level.

[27] As such, deconcentrated budget systems have subnational budget allocations rather than proper “intergovernmental fiscal transfers”. Based on historical practices in deconcentrated systems (when deconcentrated units had their own bank accounts or their own accounts within the central treasury system), the term “transfer” is sometimes still used in deconcentrated system as the (real or indicative) cash-flow transfer received within the national treasury system (or into the external bank account) from which deconcentrated units were able to incur spending commitments or make outlays. In many modern central treasury management systems, such “cash transfers” to departmental accounts are no longer needed, as payments are settled electronically within the treasury system.

[28] In some cases, the local council may actually reduce the local tax rate in response to receiving additional general-purpose grants. In other cases, the reduction in local tax collections may happen more gradually.

[29] In fact, it is quite possible that a lot of “lack of political will” to collect own source revenues is actually caused by a combination of (a) low demand for local public services by local constituents and (b) the availability of transfer resources. The impact of the transfer system on own revenue collections should be expected to be especially negative or perverse if local governments are provide with a soft budget constraint and/or deficit grants.

[30] Naturally, there is an additional incentive for over-reporting of performance achievements if frontline staff themselves benefit from better performance in the form of performance bonuses. For instance, this performance-bonus structure was the basis for (alleged) extensive cheating by teachers and educators under the No Child Left Behind Act in the United States in the 2010s (Strauss 2015).

[31] Under either scenario, however, the choice faced by the local health administrator (or the health facility head) to terminate an under-performing health worker is not just a technical decision, but needs to balance the demands of the community or facility’s governing committee; whether or not the decision will be seen favorably by the local elected leadership; and/or whether doing so would have ramifications for his or her own promotion within the sector’s service cadre.